2023: The year of pearls

With Russia: +37% - Without Russia: +39.5%

The idea of this article is to reflect on the year in general and on each position in the portfolio. Due to time constraints, I won't go through all the files or every element I add to the puzzle I'm assembling for each company, nor the PDFs I create with results or important news; I'll simply rely on my memory.

In case you're interested in understanding my investment approach and the portfolio better, I'll leave you here the interview conducted by Mr. Ciprés for the Momentum Financial channel a few years ago. It has English subtitles.

Before we begin, I want to clarify that I don't like setting fixed points in time, such as "December 31st," to analyze companies and consider stock prices. This is because each investment may be going through a specific moment in its own dynamics that has no relation to a particular date. What makes sense is to think about each company separately, understanding its peculiarities regardless of dates. However, it is also true that the investment community chooses this date for conducting this type of analysis. By thinking about each company and its processes separately, I believe I can set aside that annual calendar prejudice.

If we take all things Russian as the baseline at zero for 2022 and 2023, the portfolio's increase was 39.5%. If I consider Russia in its entirety, the increase was 37%.

What's the situation with Russian assets? All the companies are held on the MOEX through Interactive Brokers, awaiting resolution. For now, I have no intention of moving them elsewhere. The dividends haven't been credited to the account, but I include them in my portfolio's self-assessment, which I refer to as the "with Russia" calculation.

Since I began investing with Interactive Brokers following my current investment philosophy, the performance up to December 31, 2023, with full exposure to Russia, is +237%. If I impair all Russian assets in 2022, the cumulative performance decreases to +146%. I leave the assessment of performance to your judgment.

The complete portfolio at the end of 2022 and at the end of this year, to be able to see the changes, the entries and exits and the companies that are still in the portfolio.

I'll start with the companies that have exited the portfolio. I purchased Raiffeisen Bank in mid-2022 after analyzing the results and noticing that the market was anticipating the expropriation of its Russian subsidiary, undervaluing units from other countries, most of which were profitable. There was also hope for the resumption of dividends. My main idea was to have exposure to the bank because its Russian branch continued to perform very well, even better than before, as it is not sanctioned by the West and acts as a bridge between the West and Russia. However, there's also the situation that Russia does not allow it to repatriate profits to its parent company; the net profit of the Russian branch is accumulating until something changes. There were recent news updates on the issue, hence the stock had a good rebound. It was amusing to read throughout the year in the conference calls how the CEO avoided giving details about exit timelines. The results presented in 2022 and 2023 were very good in Russia and acceptable in the rest of the countries. The only problem lies in Poland, where there is a cascade of lawsuits over mortgages granted in Swiss francs. I sold with a gain of +55%. Why? Due to repeated publications from European and Ukrainian media outlets calling for sanctions against the bank.

I bought GKP at the end of last year. It seemed to me that the market was exaggerating geopolitical risk, and the dividend yield was very attractive. After delving deeper into monitoring the political situation, mainly by reading articles from local media, I decided to sell with a slight loss of 6%. The situation was much worse than I initially assessed, and this was reflected throughout the year with various issues arising with Turkey and the Iraqi government. It was a good decision because with that cash, I opened a position in Petrobras.

I had bought Polymetal because it was available on Interactive Brokers at a good price in London compared to the Moscow stock exchange; it was one of the last Russian companies they disabled for purchase. I decided to sell when the company announced that it would move its listing to Kazakhstan.

China Nonferrous Mining rose by 36.4%, including the annual dividend. It has been the top position in the portfolio since 2018. This was an interesting year because something I had been anticipating for a long time finally happened: the company increased production from its own mines. Even with copper prices decreasing, the margins were good. In terms of monitoring, the year was excellent. I had direct access to information from the Annual General Meeting of Shareholders and almost real-time information on the operations of different production units. At the Annual General Meeting, they discussed continuing to enhance shareholder remuneration. The net cash position until June 2023 continued to increase, and everything indicates that they should increase the dividend payout in 2024. What to expect in the future? Dividends and growth through investments. In recent months, they filed a note with the stock exchange stating that they expect to progress with assets that were not even known to be in their portfolio. They aim to increase production at Southeast Mine and develop Kambove West, MSesa, and Samba. There was also news that they could resume production at Shaft 28, an underground mine in Zambia that flooded in 2008. China Nonferrous continues to offer exposure to China's growth, its influence in Africa, copper, and China's effective execution in investing, as demonstrated by the track record of this company. All of this with diversified risk across various production units. It provides a good return shareholder in line with growing net profit. There is hidden value in assets that are being developed. At this pace, it will remain in the portfolio for a long time.

The Sberbank situation remains quite extraordinary. Including the 25 Ruble dividend and despite the Ruble devaluation, it increased by 69% in USD over the year. The Russian economy, despite the war, performed quite well, and this was reflected in the bank's results, which even paid out a very good dividend. The CEO has also made statements indicating they expect a good 2024. I bought them in London at a bankruptcy price and managed to transfer them to Russia on Interactive Brokers. Today, they are blocked both by the U.S. OFAC and Russia. The 1544% increase makes the wait and the risk of losing everything worthwhile.

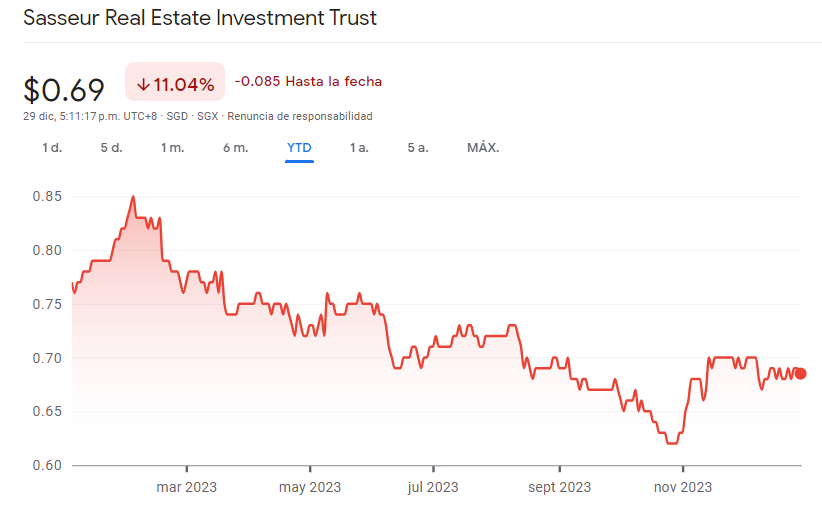

Including the 4 dividends paid, it decreased by 2% for the year in SGD. In terms of results and operations, the year was good. Liangjiang Outlet is transforming into an iconic hub for fashion and the sale of international products in Chongqing. Liangjiang are already selling above 2019 levels, while the other three outlets did not reach the 2019 volume but exceeded 2022. The occupancy rate of the premises is at an all-time high. Despite the devaluation of the yuan, results in SGD were not bad in year-on-year comparison because 2022 saw lockdowns, Covid-related reduced hours, and heatwaves. The dividend was reduced mainly due to the devaluation of the Yuan but also because of loan refinancing expenses. Another significant milestone of the year was the renewal of all loans expiring in March 2023, successfully extending maturities. Currently, there are no debt maturities until 2025. The CEO mentioned in interviews that it was a complicated negotiation process as it occurred within the real estate crisis framework, and it wasn't easy to convey that Sasseur has no exposure to the troubled sector. It was a very good year operationally, but the stock price did not reflect it, largely because it is a dividend-paying company, and the U.S. bond touching 5% sets a high bar for yields and a low one for prices. On the investor front, the tracking remains very good. I am up to date with what is happening in the outlets, primarily Liangjiang's. I managed to establish contact via email, and they even called me to clarify some questions I had sent. This month, I used dividends I received during the year to increase my position.

Since I bought Atlas Pearls at an average of 0.033 AUD early this year, including the dividend, it has risen by 471%. The AUD/USD is nearly neutral compared to the USD year-on-year. Atlas is the investment case where everything has gone well. I found it by alphabetically reviewing the Australian stock exchange in 2018. The business seemed very interesting, so I kept it under observation, even though it wasn't profitable at that time. In 2022, I noticed they became profitable because Covid forced them to sell online, increasing the customer base and creating competitive tension that led to price increases, along with fixed costs. In 2023, a wave of young Chinese buyers adopted pearls as a daily ornament. It's not just older people buying them now. You can also see images of Harry Styles or Kim Kardashian wearing them. Additionally, there is a significant reduction in freshwater pearl production in China due to environmental conservation measures. I explained this in the PDF I published on my Momentum channel. Both internally and due to external factors, everything has gone well. In my opinion, it's a very unique business, not easy to replicate. The process from the birth of an oyster to pearl production can take between 3 and 4 years if everything goes well. The supply isn't easy to increase, and we are in the midst of booming demand. The company repaid its debt, resumed dividend payouts, and plans to open a new farm in a few years. For a Micro Cap, it has been very meticulous and orderly throughout the Covid process and subsequent deleveraging. While they haven't established a fixed dividend policy, given the record-breaking results of the latest auction, there will undoubtedly be a distribution, and it will be very good. It will be crucial to understand whether the price increase is here to stay due to the China effect or if it's a passing trend. I follow daily news about the sector in China, and the appetite for pearls does not seem to be diminishing. The next auction will be in April 2024. At 0.135 AUD, I have taken some profits with 30% of the position. I have managed to establish contact with the company, and they have always responded, even on the same day when I sent inquiries.

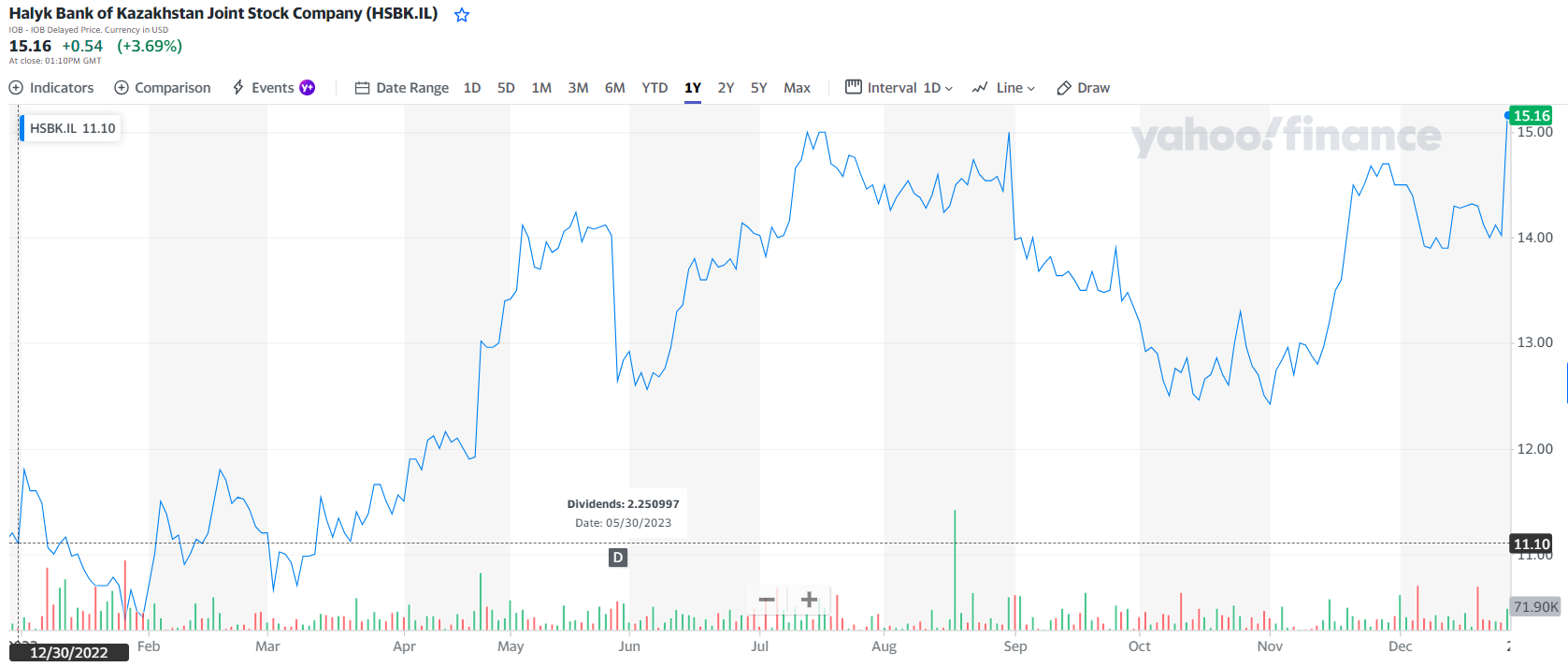

Halyk Bank increased by 56.8% in USD, including the dividend of 2.25 USD, paid in relation to the 2022 results. Halyk is the most important corporate bank in Kazakhstan. It is a serious and orderly bank that pays high dividends, with a stock price affected by the country where it operates and because the majority shareholder is the daughter of the former president of Kazakhstan. As time passes and risks do not materialize, the stock price adjusts to something more rational, and I believe that happened during this year. The bank showed very good growth in net profit, and the level of defaults remains at a healthy level. The context of high-interest rates played in its favor. The stability of the Kazakh currency, with inflation at 10.3% in November, is also favorable. As long as Kazakhstan and oil are healthy, Halyk will continue to grow at a faster or slower pace. The bank is advancing in digitalization, creating an ecosystem and an app that aims to compete with Kaspi, something I consider secondary to the main business, which is already highly profitable. They opened the "Halyk Invest" segment, offering broker services through their application, and the growth during 2023 was very good. Halyk sold its subsidiaries in Russia and Tajikistan and was in the process of exiting Kyrgyzstan; none of the three were very significant. The entire movement aims to focus on expansion in Uzbekistan, one of Kazakhstan's main trading partners. I expect the dividend to grow in line with net profit growth. The capital adequacy ratio as of September was above the level before the dividend distribution, and there is still profit accumulation until the distribution in 2024, so the dividend should already be secured. Throughout the year, I closely followed all interviews and statements from the CEO, where she makes it clear, among other things, that the bank actively works to avoid sanctions for any type of connection with Russia. She also mentions that the bank monitors each transfer to verify that there are no links to sanctioned companies or sectors that could cause problems for Halyk. Having a detailed understanding of the balance sheet and the CEO's perspective has been a significant advantage in comparison to the market and recent news concerning dividends and regulations in Kazakhstan, particularly regarding banks that received state assistance in the past. I managed to establish contact via email and was able to pose some questions during the last conference call.

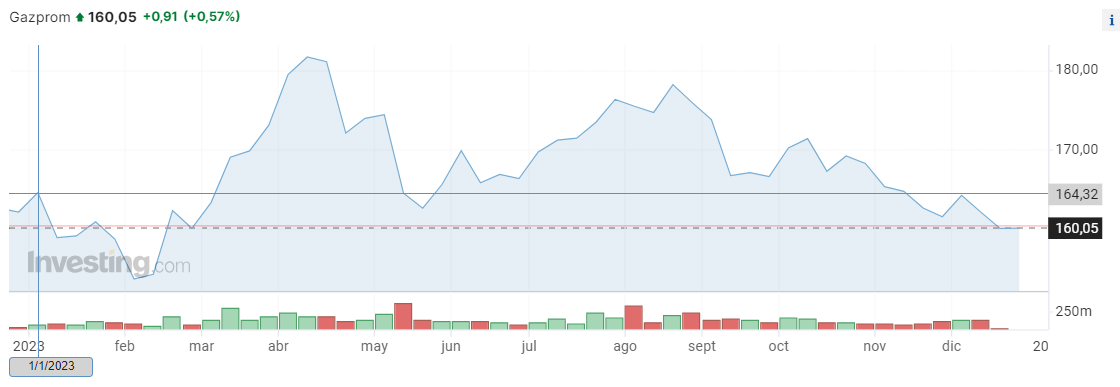

Gazprom in USD decreased by 21%. It has been in the portfolio since 2014. I believe much is already known about Gazprom's situation in relation to its main customer. Re-establishing gas sales to Europe seems somewhat distant, depending on political circumstances. The concrete fact is that Gazprom is very cheap, considering only its exports to China, some European countries, what Gazprom Neft sells, and its progress in LNG. This, combined with its sales in Russia, which are substantial. Someday, I will share an analysis of Gazprom's recent results on Twitter, and more than one person will be surprised. The local stock price is penalized due to taxes imposed last year in the context of the invasion of Ukraine and for not paying dividends this year. I have the feeling that Russian investors are waiting for the situation in Ukraine to normalize, and Gazprom returns to what it was regarding dividends. I mentioned in the program I did with Adrian that if I had access today, it's the company I would be buying the most. The shift towards the East and having 100 years of gas reserves seem like a competitive advantage and a historic opportunity. As an investor, and given the inability to buy, I have set aside Twitter monitoring since it is not of interest to almost anyone. It seems paradoxical that I have talked a lot about Gazprom on Momentum and Twitter, focusing on the advantages and the margin of safety I saw at the operational level in Gazprom. In my view, that part has been fully fulfilled, even with reduced sales in Europe. I remember doing price calculations and considering what it sold in Russia to think about a margin of safety, a floor to the price, and we won't be far from those numbers I had calculated. Time will tell if the exposure to political risk was a mistake or a success.

Kaspi increased by 35.3% in USD. Growth. Increasing dividends. Share buybacks. An ecosystem that include any business and automatically begins to grow. A company that is already indispensable for the life of every Kazakh. In the conference call, the CEO made it clear that Kaspi is not a bank; it is a Super App that focuses on data analytics to maximize income margins. They don't place Postomats everywhere; they place them where they know Kaspi customers circulate, generating automatic use of the service and increasing profit margins. The monitoring has been fantastic. There is always excellent information from Kazakh media to analyze, and I have closely followed Kaspi throughout the year for the Momentum Club. I don't like the Nasdaq IPO, but I also understand that even if the company becomes exposed to Western investors, the business remains the same. Risks? The monopoly that is being created? The perspective changes quite a bit when you follow daily statements from officials in the country.

Airtel Africa, including dividends, increased by 27% in USD. There was a crucial event for Airtel Africa, which was the Nigerian elections. The new president, Bola Tinubu, made changes at the exchange rate level, and the Nigerian Naira experienced a sharp devaluation. Even with this devaluation, Airtel Africa improved operationally to an extent that the devaluation of the Naira and other currencies did not impact the results significantly. The growth in the customer base, data customers, and Airtel Money customers shows fantastic numbers. The total number of customers compared to those using Airtel Money and the number of customers using 4G provides a good perspective on all the growth that lies ahead for Airtel Africa. In the conference call, I found it very interesting that they always provide the information on how much profit they manage to repatriate to the parent company during the quarter. Strikingly, despite ongoing challenges in Nigeria to obtain USD, the company makes it clear that they need USD to continue investing and expanding the network, not necessarily for repatriating profits. Another key point is that the CEO always emphasizes that their primary focus is on growth, regardless of whether tariffs are adjusted or not. It will be interesting to see the performance of the results and the stock in a context where U.S. interest rates have seemingly peaked.

India Capital Growth increased by 41% in USD. The fund consists of approximately 33 companies. I can only say that I am very pleased with the performance and the fund management approach, which involves minimal trading: If we compare the portfolio from last year to now, there have been very few changes. The banking sector has performed exceptionally well, as the manager consistently highlighted, particularly IDFC First Bank and Federal Bank. Ramkrishna Forgings and Neuland Labs have also experienced significant increases. As a critique, one could argue that if the fund were less diversified and more concentrated, the performance would be even better. But well... a +41% in USD... I can't complain. And since I opened the position back in 2020, the performance is even higher.

As I mentioned before, when I closed my position in GKP, I opened a position in Petrobras on January 13th of this year. Since then, the shares have increased by 58%, not counting dividends. I don't have much to comment on Petrobras. It seemed like a situation similar to Gazprom. Western investors rejected Lula da Silva in this case, as if he were an anti-capitalist president. What did it bring us? Good results and high dividends. Exposure to oil. Progress in exploration.

Consun rose by 28.8% in USD, including dividends. The results for the first semester showed good growth. The Horgos factory was inaugurated, and there are plans for the second phase to expand production. Both the risk of Centralized Drug Purchases by Volume and the Rectification in the Health System did not materialize. The risk of the expiration of the patent for Niaoduqing Granules, a recurring topic when discussing Consun, in my opinion, diminished significantly when I understood the level of competition in the Chronic Kidney Disease drug sector today. Even with competition, the Total Addressable Market (TAM) ahead is enormous: the awareness rate of Chronic Kidney Disease in China is very low. The company responded to emails with various doubts several times. The company still has a huge net cash position but pays dividends; in fact, it resumed dividend payments for the first semester, something it hadn't done in 2022. Considering its weight in the portfolio today, I believe the position is too small for the level of confidence and security the company provides me.

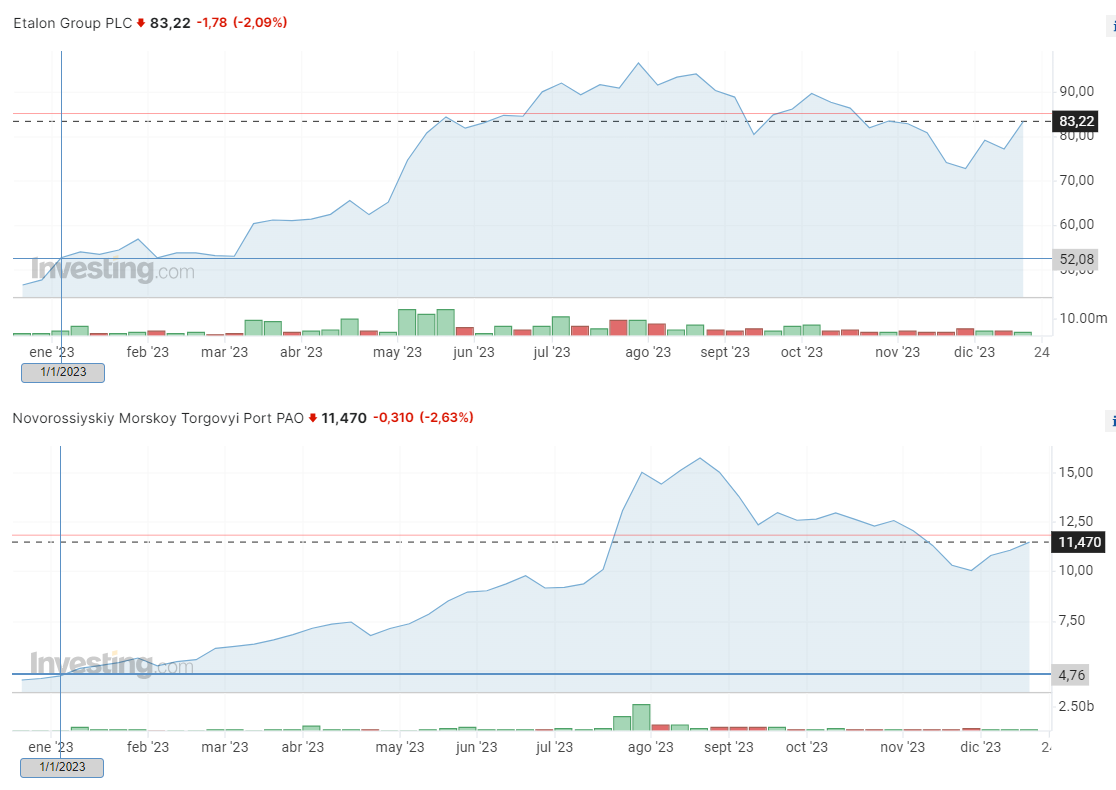

ETALON increased by 28% in USD. In terms of assets, it's a bargain. NMTP rose by 92% in USD. Russian companies that didn't attract interest even when they could be traded. Today, it's out of the question. The craziest part is that I can't help but think that if I had been able to trade, I would have made a good profit by buying during the steep decline in Russian stocks.

A new position opened this year in which I am at -20%. I never talked about it on Twitter, but it's highly discussed in my Momentum Discord channel. The company is completely overlooked on the Hong Kong stock exchange. I see it as very cheap for what it is and the operational cash flow it generates for the company and its subsidiaries. I am waiting debt reduction and an increase in dividends in the coming years.

Gemfields is another company that I opened a position this year. It is currently -16% in GBP. Mining rubies in Mozambique and emeralds in Zambia. A super serious company. At some point I will publish everything I investigated. The company repurchased 4.5% of outstanding shares at the end of the year.

Afentra increased by 40% in GBP. The company is closely followed in the Momentum Club. I liked the business model proposed by the CEO of acquiring underutilized assets and increasing their production with new technologies, something that has already been done in the North Sea but is now being implemented in Africa. His comments about "having patience" when investing in Africa convinced me that it was a company to hold in the portfolio. Production from block 3/05 improved significantly in December thanks to the applied technologies. Over time and at the pace of the Angolan government, things have gone well, and the rise over the year has been very good.

Firefinch, which owns 17% of Leo Lithium, has been suspended for over a year, awaiting the release of Leo Lithium's shares in June of this year. Most likely, after that time, those shares will be distributed among Firefinch holders, and the company will be liquidated. The Morilla mine failed and is in the process of sale, through discussions with the Government of Mali. Leo Lithium has been a roller coaster. Along with the development of Goulamina, it reached a peak of 150% before the suspension of trading due to "discussions on the export of DSO." It plummeted when it resumed trading and was then suspended again due to issues being discussed with the Government of Mali. It is still not clear what is being discussed, meanwhile, the project continues to develop. Job postings for the project are constantly being published on employment websites. In the last interview conducted from the project site, they continue to assert that production will begin in mid-2024.

TNR rose by 37% in CAD. Mariana's lithium project is progressing towards production in 2024. This would be a key milestone as TNR would start receiving cash from that royalty, distancing any dilution concerns, which are currently far away due to the partial sale of Mariana's royalty used to completely pay off the company's debt. The company also repurchased shares in recent months, but the buyback was below the issuance of shares in favor of the Directors. The Los Azules copper project is still in the exploration process and moving forward to obtain the necessary permits to begin development. A few months ago, there was a purchase offer from another mining royalty company at 0.08 CAD per share, but due to Management's refusal, the offer was withdrawn. I continue to wait for the long-term development of the projects.

Currently, I am down 16% on Playmates Toys. I delved into the investment idea presented by a Momentum user, and I liked it a lot, considering the balance, results, and the expectation that the Teenage Mutant Ninja Turtles franchise will regain the same strength it had in other times. This is fueled by the upcoming movies and series following the recent film.

The two black sheep of the portfolio: Ceylon Graphite and Evergrande. High-risk ideas with very low exposure that clearly didn't work. Evergrande was a company I bought symbolically to monitor the real estate market due to the quantity of assets it had in its portfolio. Aware that I was buying the most indebted company on the planet, I allocated less than 1% of the portfolio. Looking back, I think it would have been more useful to buy more of any of the successful ideas than to buy Evergrande, but well, experience teaches us. Ceylon promised to work on achieving low-cost production with very low Capex due to the high graphite concentration in its mines, but as time passed, production never materialized. They will remain there at the bottom of the portfolio symbolically, as they represent less than 0.5% of the portfolio.

Here are some random reflections that came to mind as I wrote all these reviews:

There are companies that have been in the portfolio for 3, 5, and even 10 years. The portfolio still has a very distinctive character, but as strange as it may seem, the focus remains on the investment being good. The "being good" part can be due to dividends, being very cheap when analyzing assets, growth potential, having a huge market to conquer, or specific advantages that, in many cases, I analyze or interpret as very favorable. In some cases, all these factors align, while in others, one or two may prevail. Take the example of Kaspi: it is a company that pays a good and sustainable dividend, buys back shares, is still cheap, has clear advantages, and is growing, besides having many opportunities for further growth. Atlas Pearls is a business with the advantage of being difficult to replicate; it will start paying dividends, was and is cheap relative to its earnings potential, but organic growth will be somewhat slower. Airtel Africa has a market of millions of people who still don't have a mobile phone for voice calls, and millions who have never had a bank account. In short, buy good businesses at a good price and wait. The key is to make an effort, always research, and try to know as much as possible.

I still believe that it is crucial for me to differentiate between saving and investing. You save for a specific goal because at a certain moment, you expect to spend that cash on something. On the other hand, you invest what is left, without specific timeframes or pressures. The freedom to invest without cash being tied to a goal gives me a lot of flexibility to operate without as many biases and concerns. I can't have an investment in a mine that has a Jihadist group 300 kilometers away and expect that I might need that cash in the short term. The lack of concern about the stock price is a significant advantage compared to the market and other investors who can't tolerate losses or buy expecting or calculating when to sell, only to later regret "selling in a hurry." The difference between saving and investing has also led me for several years to operate expecting and hoping that the prices of ideas I have more conviction in will drop so I can buy more at the lowest possible price, rather than hoping they rise. The situation in Russia doesn't pose any problem or concern for me because it's precisely cash invested, not saved for a particular purpose, and it can be lost without causing any issues for myself and my family.

I've grown tired of seeing investors trying to time the market for cyclical companies. I aim for the opposite. I go long on both cyclical and non-cyclical companies. In fact, 20-25% of the portfolio for the past 5 years is a "cyclical" company like China Nonferrous Mining that "should move" according to the copper price. But I see it differently because I don't invest in "cycles" or "sectors"; I invest in companies. The same goes for lithium. I don't invest in lithium; I was interested in how cheap the Goulamina project was when I bought Mali Lithium three years ago. I don't invest in the luxury and precious stones sector; I like how Gemfields operates. I don't invest in gold by buying 10 gold miners; I bought West African Resources because I like its mines and trust the CEO.

In many cases, knowing the companies in detail provides the advantage of adding at low points: while others sell without understanding the reasons, I try to have those reasons clear beforehand. Being informed is a great advantage and helps truly assess the risks.

I try not to "take profits" or "rotate." Usually, I don't do it, and that's causing a constant imbalance in the weights of the companies in the portfolio (China Nonferrous 20.8% - Consun 2.8%). It's not something that worries or bothers me, but I have noticed that it's an operating style that is quite unusual. I prefer to keep what works best, both operationally and in terms of price. In the case of Atlas Pearls, I sold 25% of the shares bought at 0.033 AUD for 0.135 AUD, with a 300% gain. Today, it is at 0.185 AUD. If I had sold everything, I would have missed out on almost an additional 200% with the remaining 75% of the position. I apply the "sell because it has already gone up a lot" principle to at most 30% of the position. I would consider selling more than that only in ridiculously exaggerated cases, which, unfortunately, I have never had to face so far.

I have three other positions in another portfolio: Excellence (6989 in Hong Kong), Russia's Lukoil and West African Resources (WAF in Australia).

What do I expect from 2024? To continue researching and expanding the universe of known companies. To keep tracking each company day by day to gather information and make the best decisions.

I hope you liked it. Any comment is welcomed.

Genial resglostocks! Me gusta mucho como ves el concepto de ahorrar e invertir. 💪