Tycker: KSCL - Market Cap: 30.763 mln ₹ / 307.630 Lakh ₹ / 428 mln USD

This research is by way of presentation, it does not represent a recommendation to buy or sell but an investment idea and an expression of our opinion about the company.

Kaveri seeds today is India’s largest agriculture company specializing in Hybrid Seeds in Key Indian crops. Kaveri Seed has a strong multi product portfolio of field crops and vegetables, engineered for various agro climatic zones in India and abroad.

Mr. G.V. Bhaskar Rao is the Chairman & MD at Kaveri Seeds. His agricultural family background served as grounds for his interest in farming. He pursued his graduation in Agriculture from the College of Agriculture in 1971.

Mr. Rao founded Kaveri seeds in 1976 and under his leadership, Kaveri Seeds has become a pioneer in India’s seed industry. He is a graduate in Agriculture from Andhra Pradesh Agricultural University. In 1986, his Company became as Kaveri Seed Company (P) Ltd., and in 2007 it attained the status of Public Ltd., later listed on BSE and NSE.

His foresight to uplift farming communities by developing promising high-yielding varieties of hybrid seeds has positively influenced millions of farmers. Under his stewardship the company has developed about 150 high quality hybrids and varieties across field crops and vegetables there by contributing to livelihood of farmers as well as food security of the country.

With more than 1,00,000 production growers on 65,000 acres of land across 12 different agro-climatic zones , Kaveri diverse portfolio of seeds caters to key crop segments to enable crops for diverse agro–climate and soil conditions.

PROMOTOR SHAREHOLDERS

Mr. G.V. Bhaskar Rao has 26% of the shares. Mrs. G. Vanaja Devi has another 24%.

Vanaja Devi has been associated with the Company since its inception. She is the founder Director of the Company, regularly assisting the CMD on various aspects of the business. She is a guiding force for the Company’s Corporate Social Responsibility (CSR) initiatives in the areas of rural infrastructure development and children education. These initiatives broadly include improvement of existing irrigation facilities in the rural areas, so as to improve the area under irrigation to reap good harvest, thereby improve farm yields.

Recently, the Company achieved the feat of becoming the first seed producer in India with more than 100000 acres under seed production spread across different agro climatic regions. The Company is the second largest producer of hybrid cotton seeds in India and a huge maize cob drying facility of 4500 MT per cycle.

Market standing in India

The Company has a strong presence in the domestic market and has been recording increasing growth in the exports market which includes Pakistan, Sri Lanka, Bangladesh and Vietnam.

PAN INDIA OPERATIONS

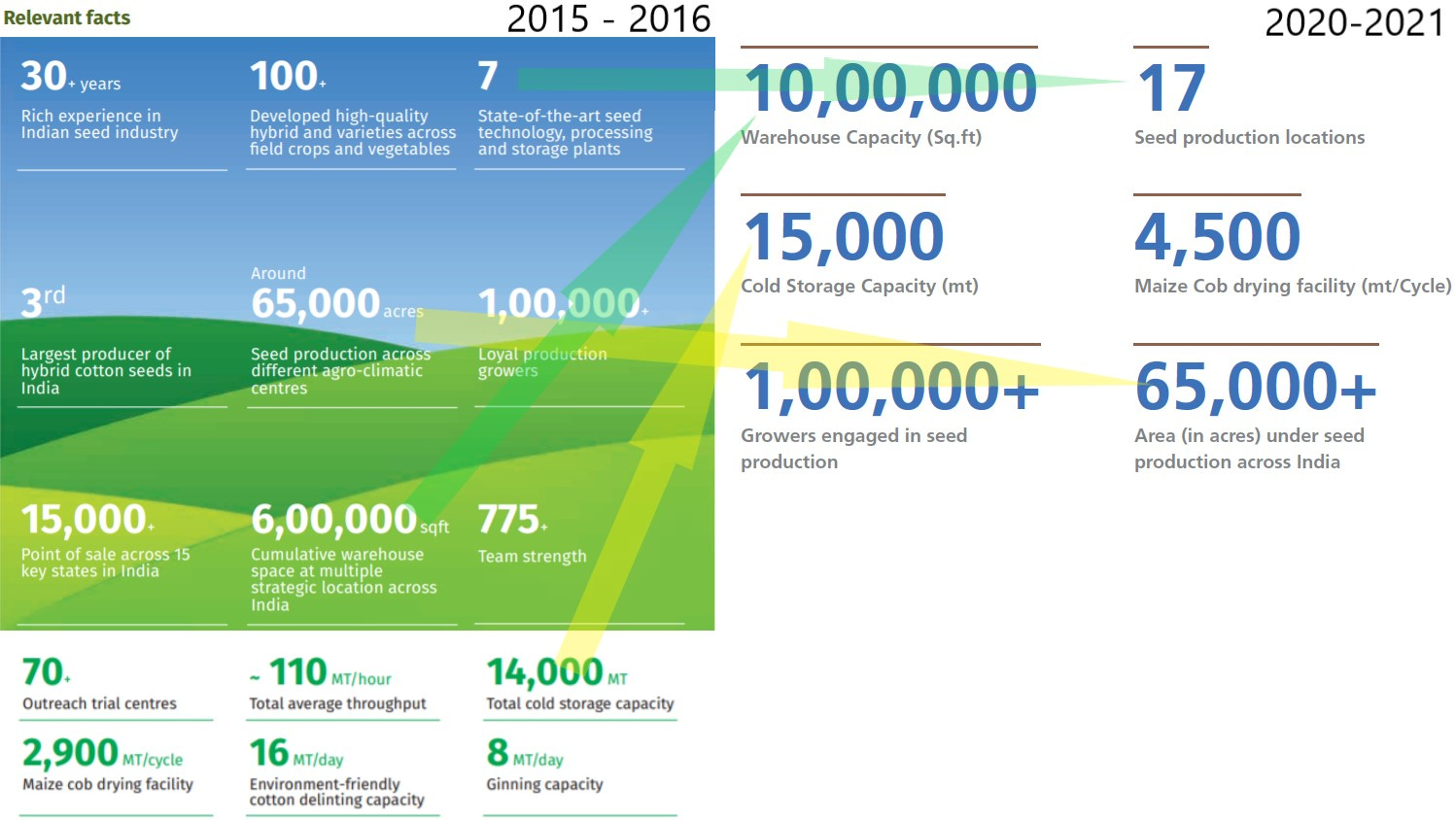

In term of storage, the Company has state-of -the-art warehouse capabilities with a combined storage space of around 10 lakh square feet which stores the seeds under ambient conditions. The Company owns 7 modern seed processing and storage plants across key locations in India which adds value to the quality and longevity of the seeds. Furthermore, the Company’s infrastructure is well equipped for ensuring biosafety including a range of green house facility for screening of pest and diseases as well as for BT Cotton containment facility.

BUSINESS MODEL

Satellite Breeding Stations of Kaveri

Based on the research gaps identified in the farmer’s field for each crop, the R&D strategy has been prepared. To meet the respective crop breeding objectives, different satellite stations were established in India. Keeping in view with region specific problems, accordingly for cotton, South Zone, Central Zone, North Zone for maize 5 stations in North, South and Western parts , for rice breeding 8 centres across the country, while for pearl millet western, southern and northern parts of the country. Similarly for vegetables at different strategic locations breeding work is carried in the country. The breeding material generated in these centres will be advanced and evaluated in the breeding trials by the concerned breeders and promising entries will be promoted to the next generation keeping in view with the desired objective. The hybrids developed in these breeding stations have to undergo through and stringent testing stages. Kaveri involve the farmers and sales team in Pre commercial stage of testing to get their feedback, which is primarily considered as an important component along with the consistency of field data before the launch of the new products.

In 2019, Kaveri launched its state of the art Biotechnology laboratory at Pamulaparthy in Telangana. The laboratory named "Centre for Applied Genomics and Seed Technology" houses the latest infrastructure and focuses on developing quality hybrids for all crops. The state-of-the-art Biotechnology lab was inaugurated by Singireddy Niranjan Reddy, Honorable Minister for Agriculture, Co-operation and Marketing, Telangana State.

Speaking on the occasion, G.V Bhaskar Rao - MD & CEO, Kaveri Seeds said, "We are delighted to inaugurate our new state of the art laboratory which significantly strengthens our research and development capabilities. We are amongst the top companies with scientific expertise to use Biotechnological tools along with advanced Plant Breeding methods. It’s always been our endeavor to innovate and we believe that the use of "Smart Breeding" will pave the way for our futuristic product innovations for high yielding, pest and disease resistant, climate- smart seeds, which will play a significant role in improving the farmer's crop yields in agricultural productivity.”

PRODUCTS

The product portfolio of the Company consists of a range of high yielding seeds in field crops viz, maize, cotton, rice, pearl millet, mustard, wheat, sorghum, sunflower and a number of other vegetable crops.

Cotton is an fiber crop of global significance, which is cultivated in tropical and sub-tropical region of more than 70 countries worldwide. The major producers of cotton are China, India, USA, Pakistan, Greece, Mexico and Turkey. These countries contribute about 85% percent to global cotton production. India is second largest producer of cotton. It plays a dominant role in the industrial and agricultural economy of the country. In India there are nine major cotton growing states which fall under three zones 1: North zone 2: Central zone 3: Southern zone. Being cash crop cotton is known for its intensive cultivation.

Rice originated in South East Asia. Agricultural population densities on Asians rice producing lands are among the highest in the world and continue to increase at a remarkable rate. Rapid population growth puts increasing pressure on the already strained food-producing resources. Rice is therefore on the frontline in the fight against world hunger and poverty. It is the primary staple for more than half the world population. Asia represents the largest producing and consuming region. In India consumer mostly prefer medium slender /short slender grain varieties. North India, hybrid rice is popular, while South India very negligible area. To make a Dent in hybrid rice cultivation in India, short to medium duration and resistant to major pests and diseases hybrid varieties with a fine grain type are needed.

Maize is the world’s primary coarse grain. It has the ability to grow in diverse climates. Its production is concentrated in North America, especially the USA, South America and China. In India, Maize ranks as the most important food & feed crop next to rice and wheat. Major course grain of corn is used for animal feed. Presently single cross hybrids with wide adoptability revolutionized the production and productivity. (Corn production has nearly doubled in the last one and half decades largely due to the adoption of single cross hybrids) .It’s penitrance to most of the non-traditional areas, thereby many fold area increased by replacing other field crops. Maize has a mind boggling multifarious end uses as food, feed and industrial by-products which is unmatched with any other crop.

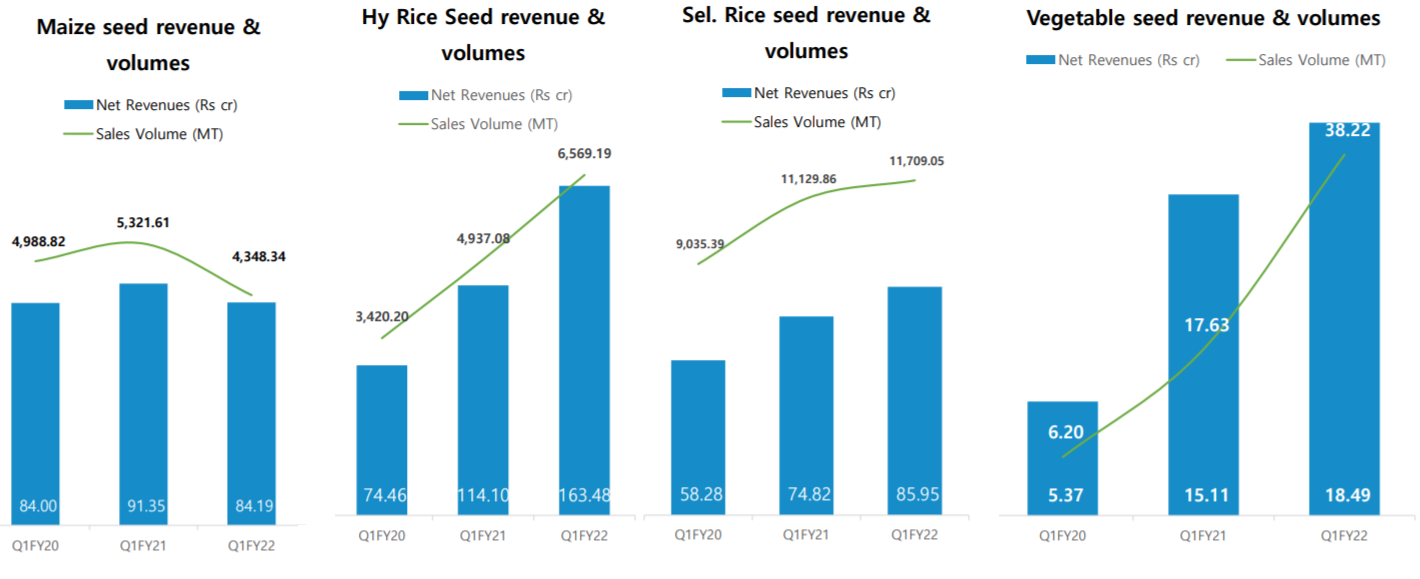

90% of Kaveri's revenue comes from these three products. 45% of the revenue comes from the sale of cotton seeds, 23% from rice and 21% from Maize.

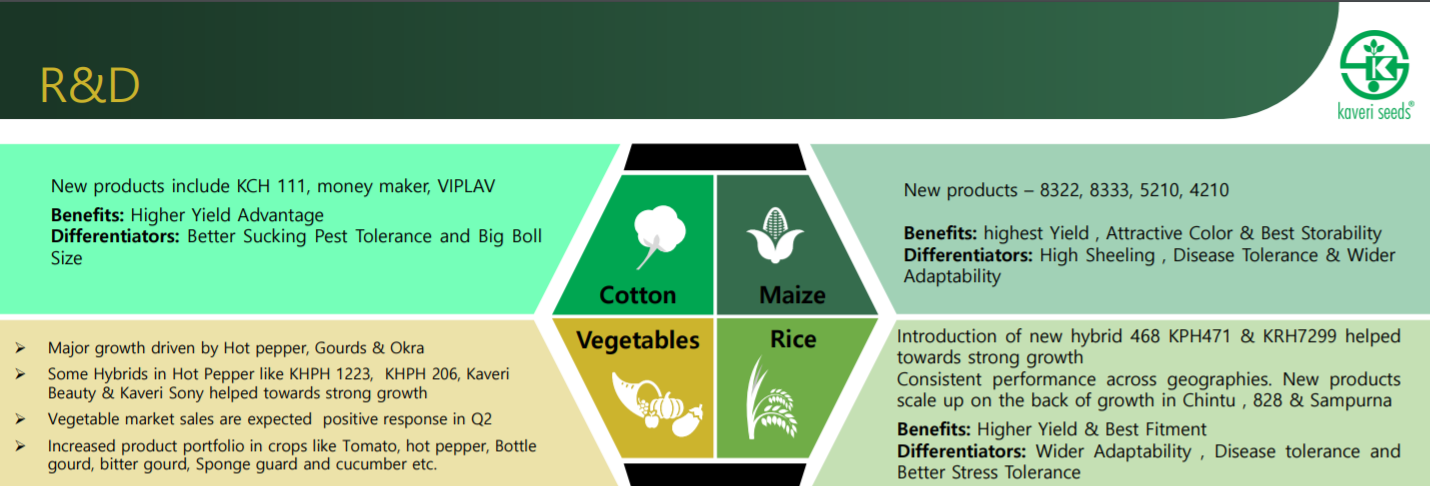

R&D

Forming the core of the Company’s business strategy, the R&D is manned by over 45 qualified scientists and team of dedicated professionals focusing on the development of quality hybrid seeds. The Company has a fully equipped State ofthe-art biotechnology laboratory along with satellite stations, strategically located for crop breeding.

The team also works on developing frontier technologies particularly in molecular breeding to augment the Company’s Germplasm which facilitates breeding programs. The Company is also equipped with state-of-the-art seed testing laboratory at Pamulaparthy. Seeds are checked for genetic and physical purity as well as germination, following the Indian Minimum Seed Certification Standards (IMSCS).

New Products for FY2021:

UNTIL 2016-2017

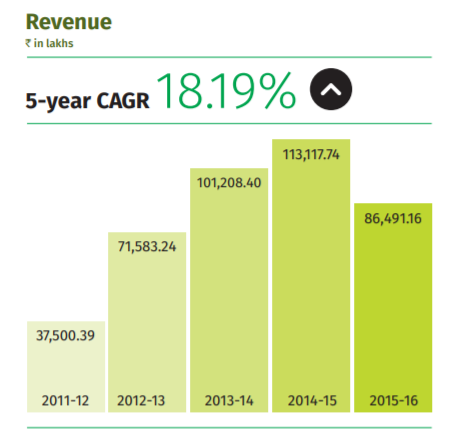

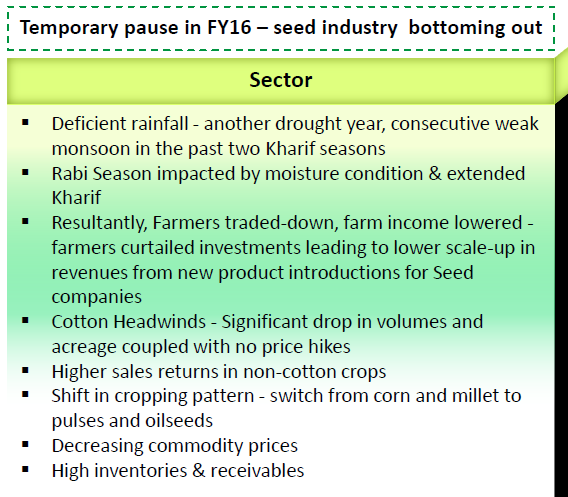

We are going to divide the Kaveri Seeds research into 2 parts: before and after the fiscal year ended in March 2017. In 2015-2016 year the revenue was reduced by 24%, after growing exponentially over the previous 3 years.

What happened in that year? The Chairman Bhaskar Rao said: “FY 2015-16 was one of the most challenging years in our corporate journey. This happened as India’s agricultural sector witnessed two consecutive years of inadequate rainfall and drought across large parts of the country. Coupled with low commodity prices, the rural sector was under tremendous stress. Given the large carryover stocks by the industry, there was significant competitive pressure by competitors to liquidate inventory. At Kaveri, we had anticipated the prevailing risks and responded with resilience and delivered a satisfactory performance, taking into account the conditions in which we had to operate.”

In 2014-15, India had a 12 percent deficit in rainfall, followed by a 14 percent shortfall in 2015-16. As per the response filed by the Ministry of Agriculture and Farmer’s Welfare, government of India, in the Rajya Sabha on the 29 April 2016, 266 districts across 11 states have officially declared drought in 2016. Some of these districts were experiencing repeated droughts over the that years (Andhra Pradesh, Karnataka, Maharashtra, and Uttar Pradesh) what leading to serious food and drinking water security concerns.

And in the framework of discussions about rate hikes by the US Federal Reserve, commodity prices were very low.

It is worth clarifying that despite the problems of the year... Kaveri did not lose money. In the operating cash flow, the increase in inventory due to lower sales is clear.

In its presentations, Kaveri shares data on the areas planted from 2016 to 2020. The fall in the area planted in 2016 was recovered in the following years, along with Kaveri's revenue.

First, we take the Area coverage during Kharif 2016-2017 for Cotton. Kharif crops are usually sown at the beginning of the first rains during the advent of the south-west monsoon season, and they are harvested at the end of monsoon season (October–November). Kharif crops stand in contrast to the rabi crops, which are cultivated during the dry season.

Cotton: From 102.8 lakh hectare in 2016 to 129.47 lakh hectare in the year ending March 2021. The area coverage by Maize and Rice did not growth from 2016 to 2021.

We have already seen that there were no large growths in the sown areas. How much did the company change from 2015 to 2021? The area under seed production is the same: 65,000 acres. The warehouse capacity increased 66%

PROFIT AND LOSS FROM 2016-2017 TO DATE

In fiscal year 2016-2017, Kaveri's revenue bottomed out. In addition to the above-mentioned droughts, the Government of India decided to set a price for cottonseed. Kaveri was down 68% from highs, anticipating the measure taken in December 2015.

“The ministry had issued the Cotton Seed Price (Control) Order, 2015, under the Essential Commodities Act, 1955. In 2016-17, Bt cotton seed prices were first lowered by a panel constituted by the Centre.” Since then, except in 2017-18, prices have been reduced.

While it must be recognized that this cap on the price of seeds would have a negative impact on Kaveri's income, it should also be noted that Kaveri enjoys benefits in relation to the payment of taxes. We see in the annual report the level of tax exemption that Kaveri had the last two years...

When India introduced income tax in 1886 under colonial rule, income tax on agriculture was kept out of its ambit because of existing land levies and the right to collect any form of agricultural income tax was vested with the main colonial administration.

In 1935, the right to land revenue, and to potential agricultural income tax, was transferred to the provinces, today’s states. Since then, each state has developed its own agricultural income- tax policy, with wide interstate disparities.

SIX YEARS LATER, KAVERI´S REVENUE RETURNED TO THE SAME LEVEL

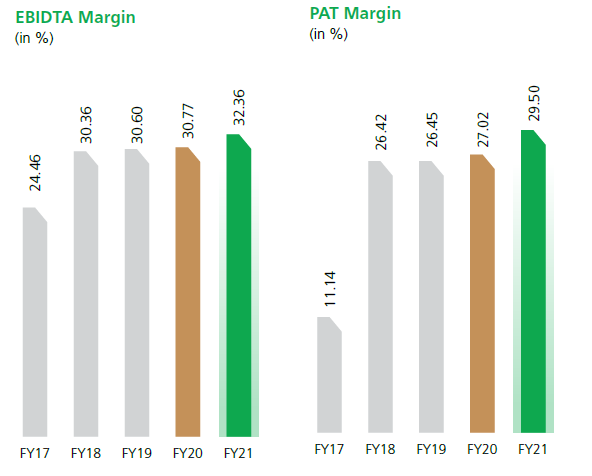

It is interesting to note that even after that measure, Kaveri's margins improved, and after 6 years since the drought and price control, the revenue returned to the same level as the 2014-2015 fiscal year.

CASH FLOW

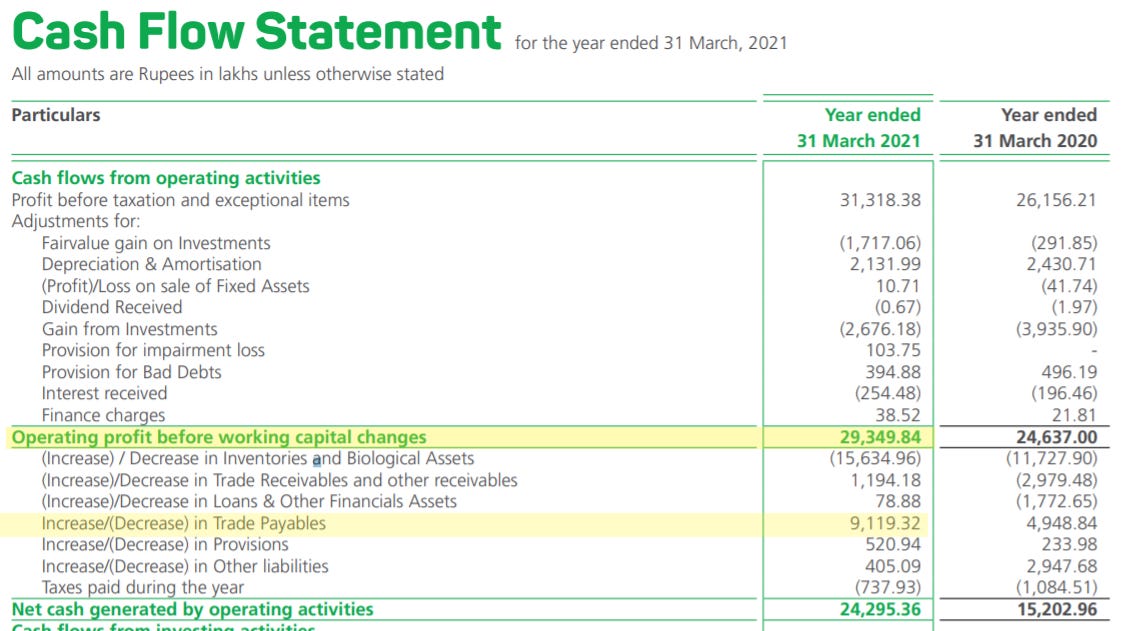

But undoubtedly the most interesting thing about Kaveri is observed in the cash flow. We want to highlight some points:

1- If we subtract the increase in trades payable from operating cash flow, Kaveri has a gain of 20,000 ₹ lakhs.

2- Looking at the cash flow from investing activities, we see a huge amount in "investments." Large amounts of investments in “purchased” and “proceeds”. During the years 2018, 2019 and 2020, the proceeds was bigger than purchases.

And this cash can be seen on Kaveri's balance sheet.

To remind later: this cash placed by Kaveri generates constant income. Where have you used this generated flow? Will see...

THE DEBT

Kaveri's debt is so low that it can practically pay all of its liabilities with the cash it has placed in investments.

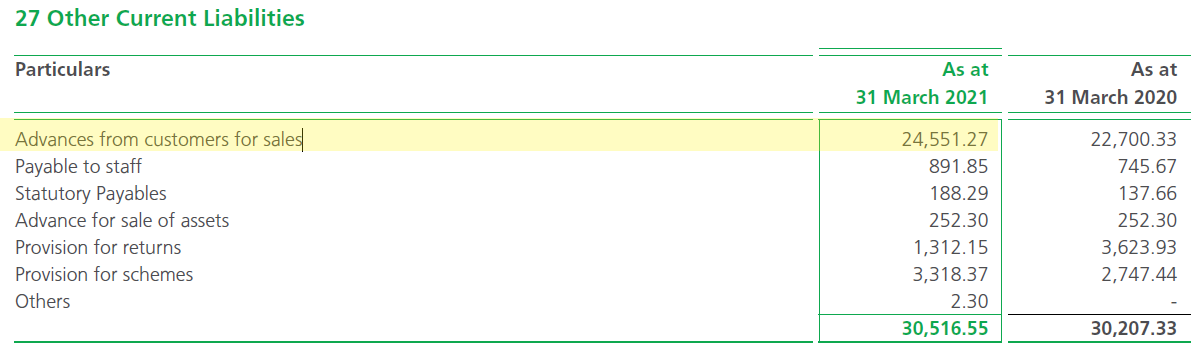

Take into account that of the Total Liabilities of 66,467 Lakhs ₹... 24,551 are "Advances from customers for sales". It is not debt, but Cash that will be released when Kaveri delivers seeds. Therefore the total debt would be around 42,000 Lakhs ₹.

Debt to equity ratio always remain next to zero…

Considering that the operating cash flow for the year ended March 2021 was approximately ₹ 20,000 Lakhs, we wonder about the value of non-current assets, valued in total at just ₹ 39,000 Lakhs...

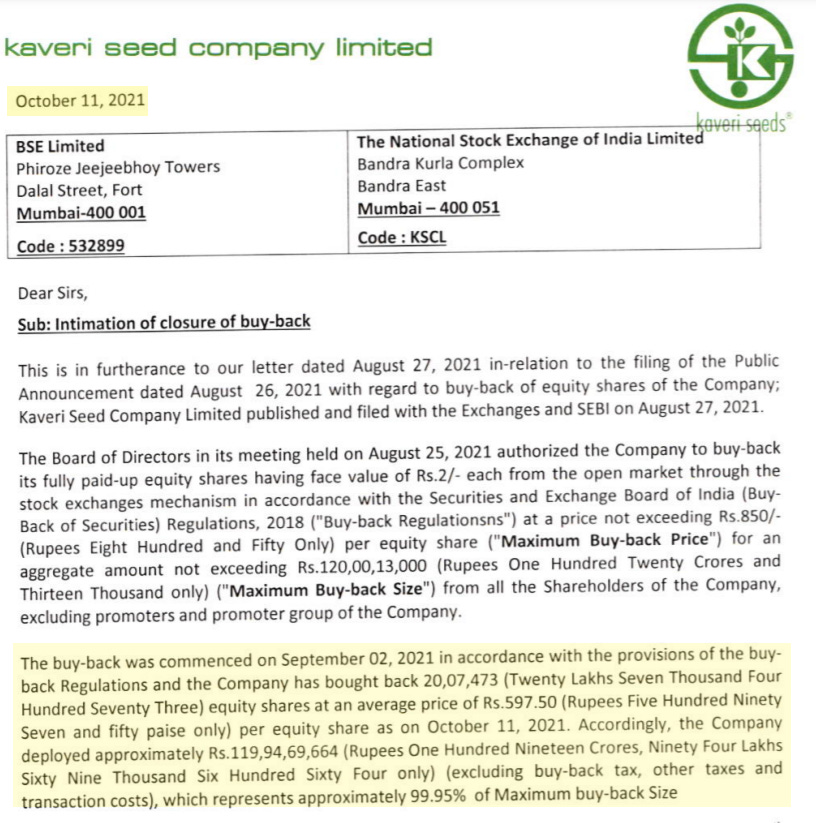

BUY BACKS

The most interesting point is that, the strength of the operating cash flow, the income from the investments that generate recurring income and the low level of indebtedness, allowed Kaveri to make quite large share buybacks.

Since FY2018 Kaveri has bought back a lot of shares.

FY 2019

FY 2020

FY 2021: During the year ended March 2021, the entire Covid year, Kaveri did not make share buybacks.

FY 2022: So far this year FY2022 the company bought back a good number of shares worth 11,995 Lakh ₹

The company extinguished 152,985 shares in October. The new number of shares is 58.321.660.

The total shares bought back after 5 years is 10.33.435 shares. This number of shares represents 18% of the current number of total issued shares.

Let us also remember that the promoter shareholders hold 57.28% of the issued shares. This means that Kaveri's Free float is only 42.72%, or 24,915,013 shares.

Therefore, the amount of shares repurchased by Kaveri in the last 5 years represents today 43% of the current Free floating!

The stock has behaved as if Kaveri had never repurchased and extinguished shares from March 31 2017 to today, and the company has spend ₹ 71,595 Lakh on buybacks! These buybacks have not led to a significant increase in Kaveri's debt.

THE SITUATION OF KAVERI'S SEED PRODUCTS

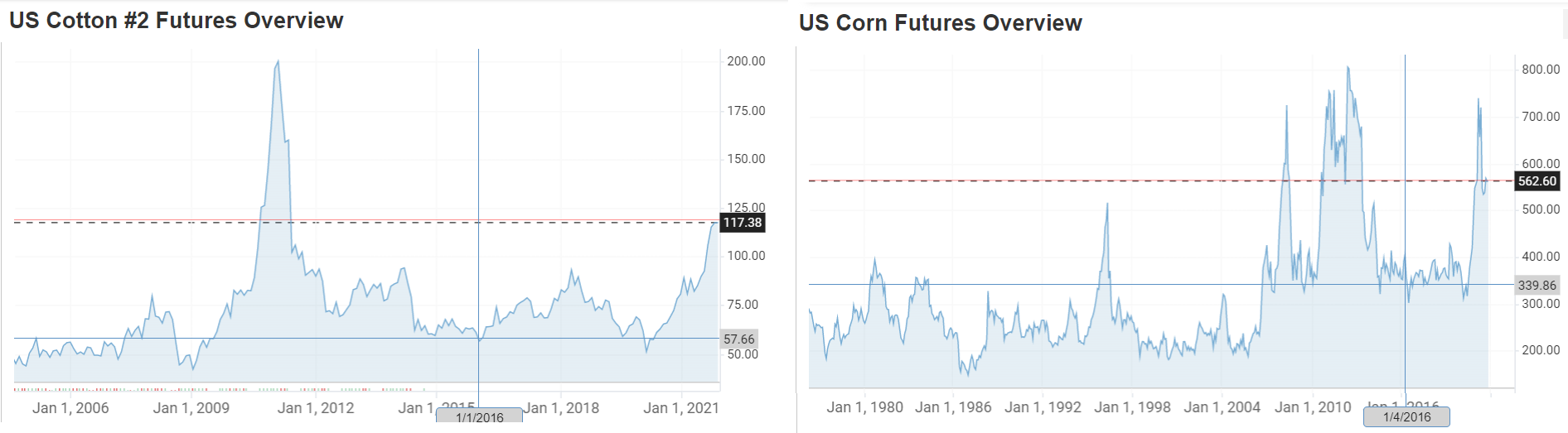

The interesting thing about Kaveri's business is that the demand for rice and corn seeds will never go away. The demand for cotton seeds may vary according to the consumption of clothing in the world.

In long term, the price of these three products is quite volatile as we have seen before. Right now the cotton is quite high by the increase in post-covid demand and the issues in relation to the ban from US to imports Xinjiang cotton.

Indias’s 2021/22 cotton consumption is forecast at a record 25.5 million bales (Mb) and exports are projected at the second-highest level in eight years at 5.8 million, according to the latest report from the United States Department of Agriculture (USDA).1

1Q FY2022

It is part of the business cycles, in this case of cotton, the situation that occurred in the first quarter of FY2022, where the revenue from the sale of cotton seeds had a significant drop.

In the Conference call they talked about that fall:

Is not the intention of ResGloStocks to analyze or attempt to follow the cycle of these commodities and of these issues that are usually presented as temporary problems. We do not want to buy sectors or have timing, we are looking for good business. We believe that Kaveri is a company to think outside the cycle. Preventing future weather is impossible, and we already know that it can have a major impact on Kaveri's revenue. Volatility and weather are real risks, but we don't see them relevant to taking a position or not in a company like Kaveri.

While cotton had these problems, rice and vegetable seeds had a good 1q.

Another interesting point is that the business has entry barriers that make the business quite difficult to repeat. Kaveri already has a circuit that is difficult to replicate.

FROM 1QFY22 CONFERENCE CALL

The conference call was held on August 16. From September 2 to October 10, Kaveri made buybacks.

The director Mithun Chand responds: “The policy remains same, in terms of the company level we want to send the cash in for the growth or as reward to the shareholders. We are exploring some options. So, for that we have held back that. If there is something material definitely we will get back to you. Otherwise, that will be returned back to the shareholder”

Mithun Chand responds: “Yes, the company is in line with your thoughts. We do not want to hold back any cash. If we do not see any opportunity, definitely we want to reward it or return it back to the shareholders. But some of the other reason, the pandemic, or some other reason we are not able to finalize some things. But as you said, we will try to take decision as early as possible because the year has also gone. So, we will definitely take this point and utter this as early as possible.”

CONCLUSION

Kaveri is a company with a business that has barriers to entry. The growth of the company is slow, but produces a necessary product for the Indian economy. Today Kaveri is traded at 15 years of operating cash flow. Generate resources with investments in financial assets. With the operating cash flow and those investments, Kaveri bought back a lot of shares.

The company is adapting to the seed demand of the producers, but the production capacity did not grow much. From 2015 to today, the area under seed production did not increase: 65,000 acres.

The debt is very low and has been low for many years, even after buying back stocks for 4 of the last 5 years.

The dividend yield is low, but if we look at it differently... Kaveri bought back shares for ₹ 11,995 Lakh in 6 months of FY2022 and distributed in dividends ₹ 2,400 Lakh for FY2021, representing a 4.7% return at current price.

STRATEGY

After looking at cash flow, debt, and the level of buybacks, we think the margin of safety at Kaveri is huge. We think that it could be a company that if it buy back shares for the same amount over the next 3 years... it could become a company that pays a very high dividend, or that the stock goes up yes or yes.

If the stock goes down, the company uses operating cash flow or investment cash to buy back. It is an investment to plant the seed, and let it grow over the years.

For us, the risk is very low, regardless of the volatility of those who operate in the short term. Undoubtedly we will see up and downs in the share price, because the market associates these companies like Kaveri with the cycles of commodities and does not look at the business, but in the long term, it seems like an investment with very little risk. If we had the ability to buy, we would have 2% of the portfolio in Kaveri, waiting for long-term growth.

MOHNISH PABRAI

We were surprised that Mohnish Pabrai had Kaveri shares in his portfolio from 2018 to 2020.

In the interview where he names Kaveri, he does not explain why he bought it. We imagine that it is for the same reasons that we are seeing. But why did she sell in 2020? We think because Kaveri is not a multibagger company. It is not at a bargain price nor is it what Pabrai calls a "spawner"2 . Mohnish is focused today on looking for such companies, Kaveri is not, but for us seems like a very safe investment in the long term.

Good write up. Who cares what Pabrai thinks about anything. His long term returns are a joke. Have you seen his indian fund pitch deck? Very misleading and doubt it had legal sign off. Guy is a clown.